A small company often does not have the assets on which to secure a loan. Banks can have a risk adverse attitude to new projects/businesses. If a business/project is considered risky, the bank may charge a higher interest rate, which a small business cannot afford, or the bank may decide not to lend at all.

SMEs particularly the smaller ones have been unable to access funds due to their limited track record, limited acceptable collateral, and inadequate financial statements and business plans.

There are only three types of financing available to a small business owner: debt financing, equity financing, or a combination of the two.

However, SMEs face challenges from limited access to finance, lack of databases, low R&D expenditures, undeveloped sales channels, and low levels of financial inclusion, which are some of the reasons behind the slow growth of SMEs.

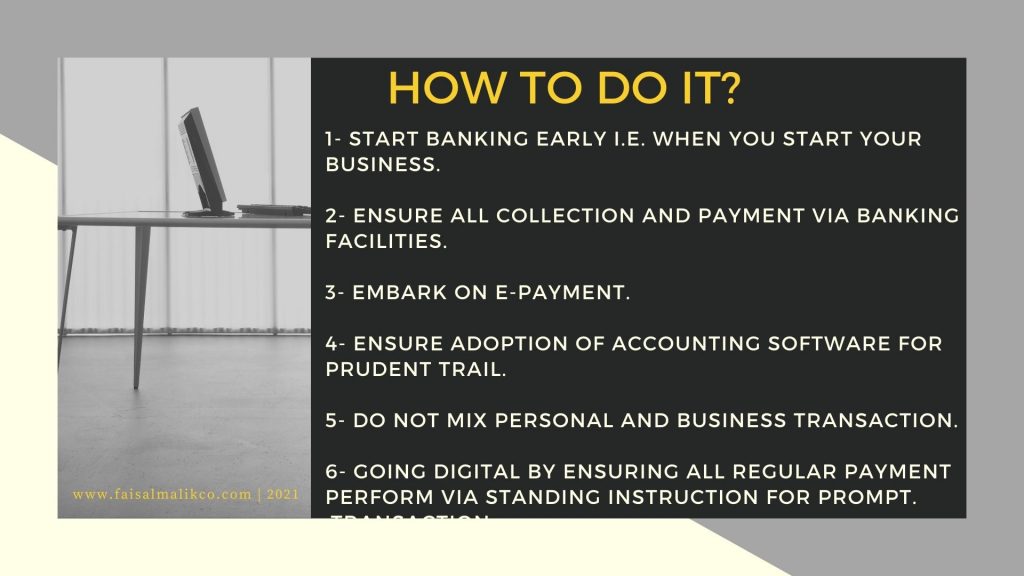

ACCUMULATED EVIDENCES HAVE SHOWN THAT FINANCIAL ACCESS PROVIDES CREDIT FOR THE MOST PROMISING FIRMS PROMOTES GROWTH FOR ENTERPRISES THROUGH THE PROVISION OF CREDIT IN THE MOST PROMISING FIRMS, ENCOURAGES MORE START-UPS, AND ENABLES INCUMBENT FIRMS TO GROW BY EXPLOITING GROWTH AND

INVESTMENT OPPORTUNITIES. HOWEVER, LITTLE KNOW OF WHAT THE BEST WAY ARE TO ESTABLISH CREDIT AND KEEP A GOOD CREDIT SCORE. SOME OF THOSE ARE: